Mobile Payment Adoption in the US: Not Yet

As any early-80’s baby, I confess to having thought seriously about the legitimacy of my faux-Australian accent. On many a Reagan-era evening, I found myself re-watching Mick Dundee outsmart yet another American criminal group, fantasizing until the day I too could sip a Fosters and audaciously mock, “You call that a knife.”

This past winter I found myself on a two-week expedition of the great down-under; finally getting to have my own up-close experience with the outback. As I stereo-typically searched for Vegemite, Weet-bix, and ‘roos around every corner, I was surprised to find that the country was far more advanced than I ever imagined. In fact, the Aussies seem to just keep outsmarting us Americans these days; at least in regards to their adoption of mobile payments.

Adoption Rates to Mobile Payments – a Comparison

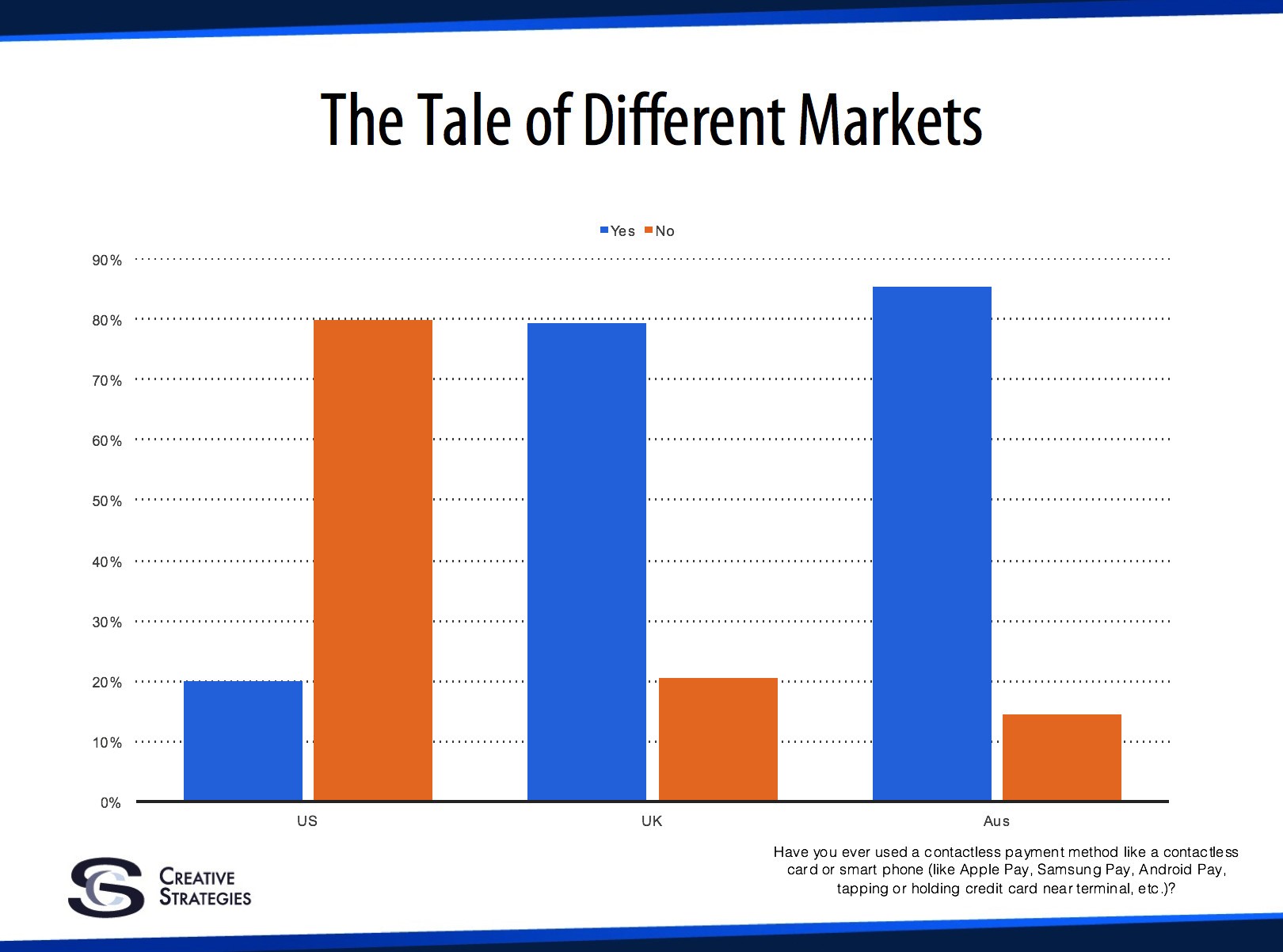

It has long been known that the U.S. lags in embracing payment advances, especially in tap-to-pay (either mobile phone or contactless card) functionality. The graph below shows that 80% of U.K. consumers and 85% of Australia consumers have used tap-to-pay. In contrast, only 20% of U.S. consumers have attempted to use this payment method. Sparking adoption to mobile payments is the fact that contactless cards (debit or credit) have become the norm in Australia. Recent data from RFI shows that in Australia 59% of consumers have utilized a contactless card for payment. In fact, tap-to-pay based payment systems have seen a surge in usage of over 200% in the last 12 months and by 2022 Australia is predicting that their country will be cash free.

In another study from eMarketer on American usage of mobile payments, it was found that just 20% of Americans use mobile payments in 2017. The article predicts that this number will only grow to 33% by the year 2020. When comprehending a statistic like this I can’t help but feel that while we (Americans) are of course very open to new technology, we do seem rather closed-minded about using technology as our payment method when compared to our peers in other developed countries. And this is an extension of the lag the U.S. experienced in wide adoption of chip technology in credit cards. In Europe, chip technology has been around for decades, but in the U.S. we have only started seeing mass acceptance of this advanced payment method since last October of 2016.

Causing a Queue in Australia

In the week I spent in Australia, I was like many other American travelers in a major foreign city, admiring the locals while holed up in a coffee shop. To my lament, I often found myself holding up the line in these cafés while I dug through my over-sized travel-bag for a wallet that was pushed well behind clothing, books and who-knows what else. After watching the locals in these same shops, I noticed that they rarely (and I really want to say never) had to pull out their wallets. I soon realized that this would have been an inconvenience for them as many of them also were pushing strollers or holding hands. When a local in Australia needs to pay their tab for their coffee they simply tap their phone to the merchants’ POS system.

Moving Up to Mobile Payments

So after watching this new payment procedure in Australia for several days, I decided to take action. This admittedly slow-to-adopt American was able to download Samsung Pay and get my credit card synced to it within a few minutes. I fumbled through my first payment; needing to be assisted by a patient Aussie teenage cashier who guided me through the simple process. However, I soon got the gist of the process and by the next day, I was tapping my phone to POS systems throughout the southern hemisphere like a true Aussie. And with my wallet no longer holding me back like George Costanza in a Manhattan diner, I felt a new kind of freedom.

Teaching Cashiers in the U.S.

The middle-aged woman working at the Phoenix area convenience store stares at me blankly as I hold the cold can of exertion-inducing energy drink. She appears ready to yell, “Are you going to pay me or what?”

I again am using the Samsung Pay app which I have expanded to a few of my highest used credit cards. I place my fingertip on the sensor on the back of my Galaxy S8 and it vibrates indicating that I have 15 seconds to tap it to a POS with mobile payment functionality. I hold it to the card-reader as the woman glares disbelievingly at me wondering how I expect to make a payment without a card. I momentarily wonder if she glares like this at home, waiting for her kids to put their toys away. I snap out of my daze having received the confirmation phone vibration and accompanying notification from the app confirming the payment has been completed. Smiling, I look up at the suddenly-interested woman who is baffled by the strange payment transaction she has just witnessed. Intrigued, she states matter-of-factly, “I have never seen that before.”

Upon arriving home from Australia I continued to try to use my mobile payment app. However, I found that almost every vendor that actually had the Mobile Pay Accepted sticker on it was not sure how to use it. In fact, I was almost invariably the first experience of a customer actually utilizing mobile payments for each cashier I interacted with. These clerks reviewed me quizzically as I showed them how to use their own POS system. At this point in July 2017, I have likely been the first mobile payments transaction for at least 30 salespeople in the few months since my return. And this includes stores in major metro areas in Arizona, Ohio, Texas and many areas in between.

The Future of Mobile Payments in the US

I have no doubt that mobile payments will become the payment method of choice in the U.S. However, based on the early adoption of this system and the lag in widespread usage of chip technology it could realistically be 5-10 years before we see this play out across the U.S.

Now as I check out at my local gas station, brewpub, or urban coffee bar I can still feel like an early adopter, proud of myself as I sip my macchiato that I did not wait for this payment technology to become widespread. Will it take the time of an extended Dundee-esque walkabout for this technology to become ubiquitous in this country? Time will only tell.

Mobile Payments in the US References

https://www.recode.net/2016/9/28/13067218/mobile-payments-contactless-tap-to-pay-apple-android\

http://www.abc.net.au/news/2016-08-01/australia-embraces-tap-and-go/7676816

https://www.emarketer.com/Article/Mobile-Payments-US-Growing-Fast-Still-Far-Mass-Adoption/1014689

https://www.emarketer.com/Article/Mobile-Payments-Will-Triple-US-2016/1013147

https://www.linkedin.com/pulse/cashiers-last-stand-chip-cutter

https://www.chasepaymentech.com/faq_emv_chip_card_technology.html

https://thefinancialbrand.com/62691/mobile-digital-payments-usage-awareness-iot/